The currency markets have been almost completely absorbed in two major developments. The first is

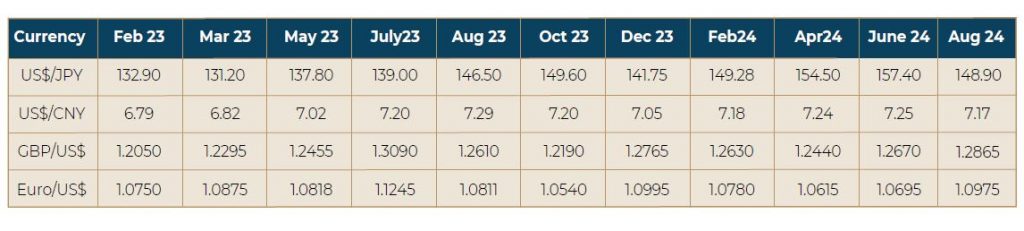

related to the Japanese Yen. The Yen weakness against the US Dollar taking it to the 160 mark, and the

subsequent strength of the currency to the 148 level in a rather short span of time has been at the centre stage. The economy of Japan reported growth for the last two quarters, and this gives the comfort that the economy is in a revival mode after almost three decades of sluggishness. The Bank of Japan hiked the base rate, and with growth coming back in some measure the BOJ is expected to hike the rate further. This has lent immense amount of strength to Yen.

But there is some amount of political uncertainty surrounding Japan as there is news of the current Prime Minister Fumio Kishida not likely to seek re-election in the September elections, ruling him out as the Prime Minister for an extended term. In Japan by the very nature of the polity and the economy quite a lot of things revolve around the persona of the Prime Minister.

A second, and probably more important factor, to reckon with is the developments in the US. With

inflation moderating, the likelihood of a rate cut in the US is placed as a high probability by majority of

analysts and Fed watchers. This move which is potentially a September event may push the US Dollar

lower, and this may also help Yen to strengthen further. Unlike at any time in the past the Fed action

seems to be a certainty, and the US markets too are pricing in the same especially in the treasury yields.

The Rupee may slide as the pressure on account of payables, mainly imports, will put pressure on the

currency. There is no relief that trade can offer. However, even with inflows in case the RBI goes into buy Dollars from the market it may prevent the Rupee from appreciating beyond a level like US$ = Rs.83.30/60. The exit by overseas investors from equity is also adding to the woes of the Rupee, and the currency may remain relatively weaker as we gradually move into the festive season.

Japanese Yen mainly represents the Eastern Currency Bloc with an active currency market, and one of

the largest bond markets taking into consideration both the Japanese Government Bonds and Euro-Yen Bonds. Therefore, the currency has an important place as a reserve currency. Japan enjoyed a trade surplus with the US for the last 100 years and this has been the determining factor behind the Dollar-Yen exchange rate. Adverse currency movements which result in an inflation of the trade surplus naturally makes the US a bit concerned. But a change that has happened in the recent years is that China has replaced the US as Japan’s leading trade partner. Despite the hike in the base rate by Bank of Japan, the market rates still continue to be quite low, and they may not edge higher too soon as the Japanese markets are extremely orderly and well-studied in their movements. The relative attractiveness of swapping non-Yen or other-currency loans into Yen-denominated loans still looks an attractive proposition for those who may hedge the currency risk and also for those who have natural hedge through Yen receivables. The bulk of such trades may not cause any disruption in the markets.