The fixed income markets continue to remain more or less range-bound, eagerly waiting to factor in the probability of any future rise in interest rates. There is more or less agreement among the market participants that rates should rise at some point in time during the course of this year, but the question is when? What adds to the difficulty is the inability to estimate the after-effects of the second wave of the pandemic on output employment and price level. We may have some idea about this only after we start getting the actual numbers. Given the fact that the situation is under control, though many major cities are still under some amount of lockdown, the damages could be limited compared to the first wave. Inflation indicated by the CPI is within the target levels, but there is going to be a certain rise in the price level resulting from the high oil prices in overseas markets. The rise in petrol and diesel prices have a cascading impact on the prices of all essential articles and consumables through higher transport costs. Even with the is rise inflation may be close to or around

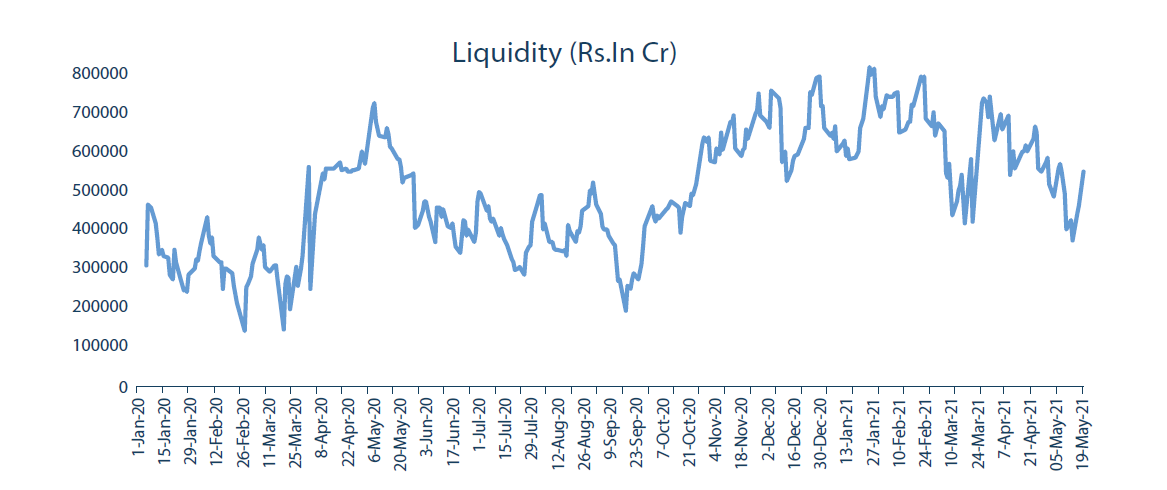

the RBI’s target level. Any breach of these levels may have implications for policy. In the recent policy announcement, the central bank has given ample indications of continuation of the accommodative policy the hallmark of which is the liquidity policy. But the inherent limitation is the price level and the rate of economic growth. Any pick-up in these two variables could be the swansong of the accommodative stance. What may afford the long end of the curve relative stability is the GSAP1.0 which is for Rs.1 lakh Crs in Q1 and the recently announced GSAP 2.0 which is to the tune of Rs.1.20 lakh Crs. These measures may bring in greater comfort to the market participants that the government borrowing programme may not be very disruptive and that the issues may sail through smoothly. The borrowing programme being massive with close to Rs.12 Lakh Crs being mobilized from the open market, it is not going to help rates to come down. The environment globally too is one of high growth with high inflation, and this may also have some bearing on the aspects of policy formulation in the domestic economy. The US and Europe are both moving into faster growth and higher inflation, and the accommodative policies pursued by them may also undergo revision in the near future, which may compel some policy modifications in other larger economies too. From an investment or portfolio perspective, the short end of the curve is the best destination, and the very short maturities make better sense given the expectations of an eventual rise in rates during the course of the year. It is also important that the credit profile of the portfolios should be of high quality and there should not be any compromises on this count given the fact that there are more downgrades than upgrades in credit ratings since late 2019. Portfolio quality should be uppermost in fixed income allocations.

In fixed income, it is still the short end of the curve that is preferred. Even those who are invested into the short end may gradually move into the very short end over the next two or three months, to avoid any loss of value due to a gradual rise in rates, owing to normalization of liquidity and economic conditions, most likely over the next three to four months.